A notary public acts as a signing agent, or a person authorised to witness the signatures on various kinds of legal documents, including mortgage loan documents. Most banks offer notary services to regular customers during normal banking hours, as another way to provide personalised customer service. Having a notary public on staff is not only convenient, but is considered by many banking customers to be a professional courtesy.

Features

Notary services provided by banks, credit unions and other financial institutions include certifying documents for the purchase and/or transfer of real estate, mortgage loans, refinance loans, equity line of credit, deeds, escrow documents, trusts, powers of attorney and wills. Considered to be an impartial witness and officer of the law, a notary public is appointed by a state government. In many states, applicants are required to complete special training and pass an exam before final appointment.

Significance

Because of the number of property transactions in which they are involved, many banks have a notary on staff during normal business hours. Banks also offer services such as setting up living trusts and other trust accounts, estate settlement and investment management, all of which require signatures on documents. The role of a notary public frequently involves assisting lenders, banks and title companies by ensuring that borrowers sign, initial and date all loan documents where required per the lender's specific instructions.

Types

While most lending institutions have a notary public on staff, many utilise the services of a mobile notary-public service. A key advantage offered by a mobile notary is that she sees the customer at a location and time convenient to both lender and borrower.

Function

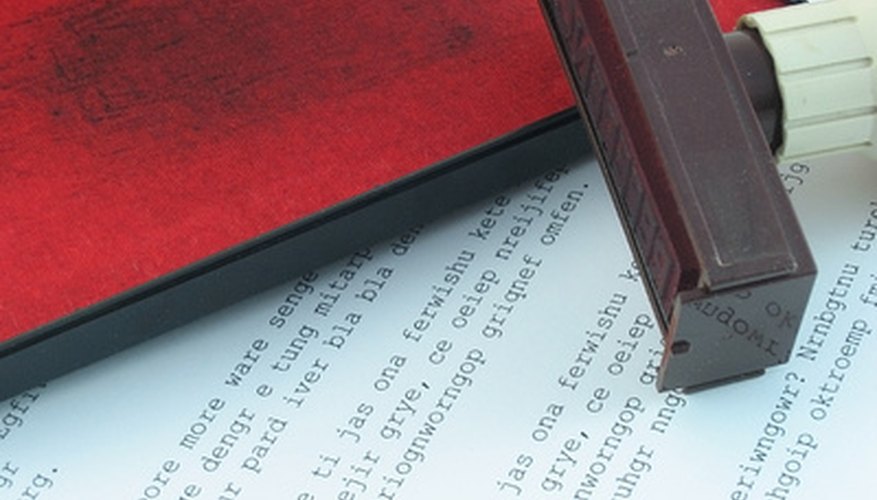

Certain legal documents require signatures to be witnessed by a notary public, to prevent fraud. A notary public must request proper identification before witnessing a signature on a document. The notary asks to see photo identification that also includes a physical description of the person, as well as the person's signature. A driver's license or passport is the form of I.D. commonly used for identification purposes. A military I.D. is another form of identification that is accepted. Once the notary is satisfied he has obtained proof of the identity of the person signing the document, the notary is then required to witness the signing of the document before he dates and signs it. Finally, the notary public affixes an embossed seal or stamp to the document. This seal attests that the person named in the document is the person who has actually signed it.

- Certain legal documents require signatures to be witnessed by a notary public, to prevent fraud.

- The notary asks to see photo identification that also includes a physical description of the person, as well as the person's signature.

Misconceptions

Notarising a document does not make it legal, but rather certifies that the person signing the document appeared before the notary. The job of a notary is to witness a signature rather than a document; therefore, he/she is required to know the purpose of the document, in addition to understanding how the document is to be completed.

Warning

A notary public may neither be a party to the transaction nor have any financial interest in the transaction. Since most notaries are not attorneys, they are prohibited from offering legal advice or explaining any of the information contained in the documents. While a notary public may not answer specific questions about a loan, and is not permitted to actually prepare loan documents, he/she may point out where in the document important facts of information are located. Notaries may not notarise documents that are incomplete, copies of documents (except for Power of Attorney) or signed documents that have been faxed. A notary public officially validates the identity of the person signing a document, witnesses the signature, completes the notary information on the document, and then affixes the notary seal. Notarization does not prove that statements made in the document are true.

- A notary public may neither be a party to the transaction nor have any financial interest in the transaction.

- While a notary public may not answer specific questions about a loan, and is not permitted to actually prepare loan documents, he/she may point out where in the document important facts of information are located.

Considerations

Any documents that are notarised must include the printed name of the notary, the notary's signature, the date(s) the documents were notarised, and the expiration date of the notary's commission. He must be at least 18 years of age and a resident of the state where he/she is commissioned. A notary public may not have a criminal record. In some cases, a notary may not necessarily reside in the state where he was appointed; however, he/she must be employed in that state. The State Senator from the applicant's senatorial district is usually required to approve the application before an appointment is made. Documents are sealed with the notary's official seal or rubber stamp and then recorded in a journal the notary keeps as a permanent record. The notary public's register should include the type of official act performed; the name and address of the person requesting notary service; the date of the transaction; how the person signing the document was identified; the type of document certified; and any fees charged. Information on the notary seal includes the name of the notary, the words "Notary Public" and the county in the state where the notary is commissioned.

- Any documents that are notarised must include the printed name of the notary, the notary's signature, the date(s) the documents were notarised, and the expiration date of the notary's commission.

- Information on the notary seal includes the name of the notary, the words "Notary Public" and the county in the state where the notary is commissioned.